We have complied a list of related creator economy research to help you on your journey. And be sure to check out The Tilt’s original Content Entrepreneur research updated yearly.

Creator Economy Benchmark Research published by The Tilt (2022)

New research on what it takes to be a content entrepreneur

The Tilt surveyed over 1,000 content creators to learn what motivates them, how they build a successful content business, and how quickly they hit key business milestones. All the findings are summed up in a report called The Creator Next Door, commissioned by The Tilt.

Key Findings:

- More than half of full-time content creators are self-supporting (i.e. supporting at least one person). And nearly 1 in 5 say they earn “substantial” income.

- Full-time creators need roughly 17 months to earn enough income to support at least one person. And they tend to bring on outside help at the 25-month mark.

- Just 1% regret their decision to become content creators. This group is overwhelmingly satisfied with their decision to become creators – and this finding holds true regardless of the number of years since they’ve launched their business and the amount of money they earn.

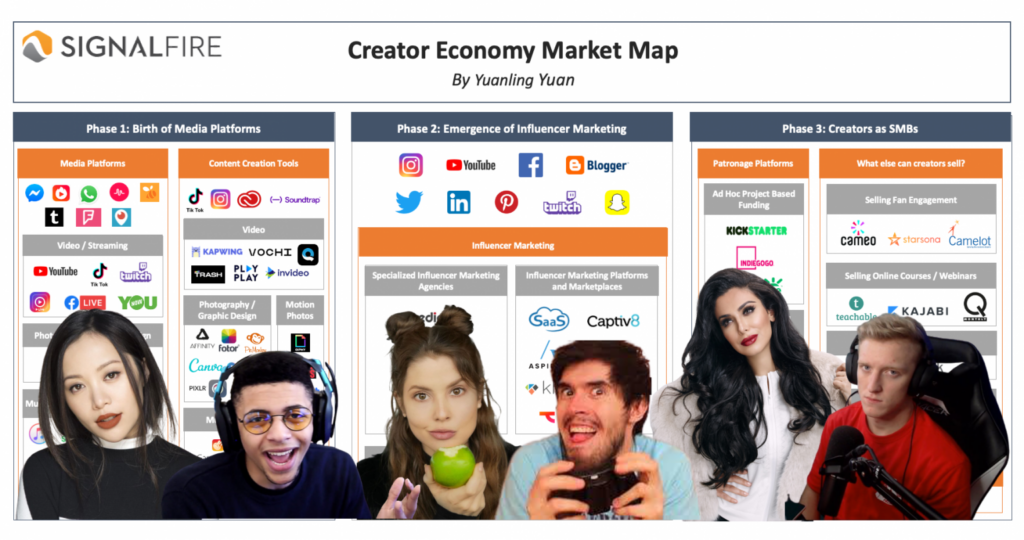

Creator Economy Market Map published by Signal Fire (2020)

Often cited report that indicates size of creator economy. Also includes the multiple layers that lead to creator businesses along with pros and cons.

Key Findings:

- 50 million individual creators determined by size of social media account followers.

- 2M+ full-time: 1M on YouTube, 500K on Instagram, 300K on Twitch, and 200K for other (musicians, podcasters, writers, etc.)

- 46.7M part-time: 31M on YouTube, 30M on Instagram, 3M on Twitch, and 2M for other

Tilt Take:

The 50M size of the creator economy is woefully underestimated. It seems to all but ignore those creators who aren’t on YouTube, Instagram, and Twitch. We also question how audience size is the only factor in calculating whether they are part- or full-time businesses. On the bright side, the 50M is impressive enough to garner global attention to the industry’s potential.

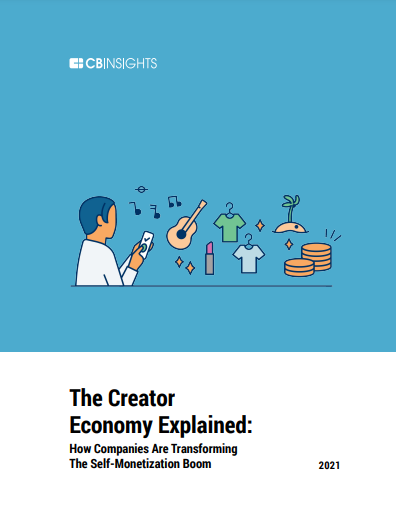

The Creator Economy Explained: How Companies Are Transforming The Self-Monetization Boom published by CB Insights (2021) [GATED]

Dig into how creator economy startups are building across the value chain, top investors and companies in the space, and what’s next for the industry.

Key Findings:

- Greenfield opportunities lie in building out the ecosystem around creators as founders.

- Research identifies 125+ creator-focused companies capitalizing on each step of the creator work cycle.

- Creator-focused companies featured in CB Insights’ creator economy Collection have reaped $1.3B in funding in the first six months of 2021, nearly triple last year’s $464M.

- Valuation of unicorn status companies: Patreon ($4B), Kajabai ($2B), Cameo ($1B), Substack ($650M), VSCO ($550M), Splice ($550M).

- Opportunity for platforms that address middle-class creators, providing opportunities for anyone to grow and succeed.

Tilt Take:

The creator economy isn’t just about the creators. It’s all about all the existing and potential businesses that can help those creators. The big investment in businesses that serve creators indicates the long-term power of the creator economy.

Creator Earnings: Benchmark Report 2021 published by Neoreach in partnership with Influencer Marketing Hub (2021) [GATED]

Survey and conversations with over 2K creators to learn more about how they monetize their followers is in this creator economy research.

Key Findings:

- 46% of Creators who have been building an audience for 4+ years earn over $20k annually across their monetized channels.

- Of creators who say content is their main source of income, 78% make $23K+ annually.

- 77% of creators depend on brand deals (3x more than every other revenue source combined.)

- Follower count and income are not directly correlated. Creators earning $50K to $100K have an average 1.8K fewer followers than those earning $500k to $1M.

Tilt Take:

The survey focuses on creators who primarily use social media. It indicates the real challenge of upping your content business to make a living that can support your household. It also shows the value of building an authentic audience, not just boosting your follower counts.

The Creator Economy Report published by The Influencer Marketing Factory (2021) [GATED]

Surveys of 600 social media users and 500 social media creators to assess monetization on the platforms.

Key Findings:

Among the user findings:

- 63% of users had tipped a creator at least once. Of those, 37% usually tip nothing, while 18% usually tip $10 to $20.

- 58% say they are interested in paying a subscription fee in the next year to receive exclusive content from their favorite influencers, with 23% indicating they would pay $4 to $7 a month.

Among the creator findings:

- They’re evenly split on the platform where they make their most money – TikTok (24%), Instagram (22%), and YouTube (20%).

- Their annual revenue breakdown: Less than $20K (41%), $20K to $50K (20%), $50K to $100K (18%), $100K to $500K (13%), 8% $500K+.

Tilt Take:

Seeing both the user and creator perspectives are invaluable to figuring out the best business strategy. Exclusive content can be a good opportunity for creators to launch paid modestly priced monthly subscriptions.

The State of the Creator Economy: Assessing the Economic, Cultural, and Societal Impact of YouTube in the US in 2020 published by Oxford Economics (2021)

YouTube’s creative ecosystem contributed $20B to the U.S. economy in 2020, the equivalent of 394K full-time jobs. This original creator economy research includes a survey of creators on the platform. It is told through stats and narratives from some of those creators.

Key Findings:

- 66% of creators with 50K+ subscribers say they can build a self-sustainable business on the platform.

- 57% of creative entrepreneurs say YouTube brought them additional opportunities away from the platform.

- 80% of creators agree YouTube helps them reach international audiences they wouldn’t have access to.

- 73% of creators who average at least 35 hours per week on their channel agree the YouTube community encourages them to create “diverse and innovative” content.

Tilt Take:

The survey-based approach reveals some interesting stats and stories. We were particularly interested that over half of the creators found YouTube can be a conduit to other revenue streams. We’d like to see that number grow. Creators should take advantage of the opportunities on platform, while also building audiences and earning revenue off site too.

The Creator Economy by Oxygen published by Oxygen (2021)

Brief survey to understand generational involvement in creator side hustle.

Key Findings:

- 88% of all surveyed consider themselves a creator or freelancer, including 78% of Boomers, 87% of millennials, 91% Gen X, and 93% Gen Z.

- Over half say they have made money from their side hustle. Only 20% say they are bringing in enough to make it a full-time business.

Tilt Take:

Creator-based businesses aren’t limited to the younger generations. But while many consider themselves creators, few make enough so it can be their full-time business.

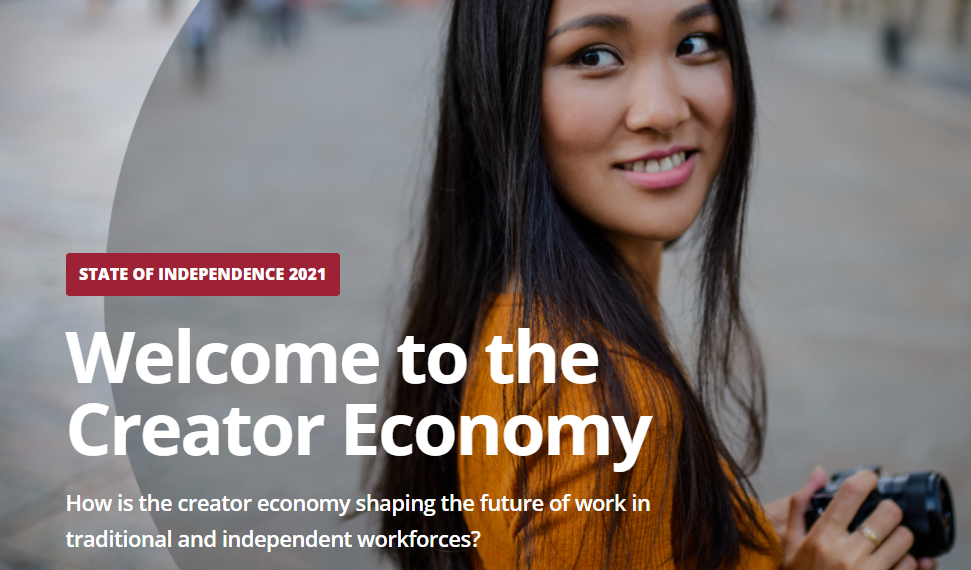

State of Independence 2021: Welcome to the Creator Economy published by MBO Partners (2021)

Research shows 7.1M creators earn income from their work; survey explores their digital content creation and monetization activities.

Key Findings:

- 7.1M earn revenue, while 4.4M work as creators but have not yet earned income.

- 59% also have a traditional job.

- 55% team up on projects with other content creators

- Percent of creators identifying as Black (19%) is more than percent of U.S. population (12%).

- 36% hire contractors to help in their business 6. 34% struggle with boundaries and burnout

Tilt Take:

These findings encompass the operationalize side of creators running a business. Partnering with other creators can be an opportunity to boost your value by combining your audiences to expand the reach of your creations. Creators also are willing to hire people to help on the business side of things.

The State of Influencer Equality 2022 published by IZEA (2022) [GATED]

Analysis of IZEA data for marketplace transactions (over $60M) to influencers broken down by age, race, gender, including costs per posts, platform details, etc.

Key Findings:

- Sponsorship deal flow for racial minorities now exceeds their share of the U.S. population.

- Females dominate influencer marketing with 83% of transaction volume in 2022, but their share is the lowest it’s been since 2015.

- Influencers over the age of 65 earn three times more per post than those 45 to 54.

Tilt Take:

Research like this lets you dig into the details behind general creator economy headlines. It can serve both as a benchmark for your current content business and an opportunity to reflect on the creator community’s diversity and inclusivity.